AI capex arms race continues to accelerate. The companies that build and supply compute will dictate access, pricing, and deployment speed.

Summary

Are Big Tech’s vast AI capital expenditure programmes laying the foundations for a genuine productivity surge, or sowing the seeds of the next bubble? Each new spending announcement still triggers reflexive comparisons to the dot-com era, yet those analogies increasingly miss the point. AI has transformed compute from a utility into a strategic asset. Strategic assets are never about shared access. They are about control.

The companies that build and supply compute infrastructure will dictate access, pricing, and deployment speed. Control the bottleneck and you control the economics of the entire ecosystem layered on top. That reality explains why the AI capex arms race continues to accelerate, and why simplistic bubble comparisons fail to capture the scale of what is unfolding. This is no longer about individual winners or losers. OpenAI’s eventual fate matters far less than the structural shift now underway.

The investment framework around capex is changing. Markets currently focus on hyperscaler margins and near-term free cash flow. That focus will move toward a more consequential divide: companies with secured compute access versus those forced to rent capacity, absorb hyperscaler margins, and operate with structurally higher costs. In an AI-driven economy, control of compute is not optional. It is decisive.

Against this backdrop, changes at the Federal Reserve and a renewed policy push toward deregulation and growth signal a potential inflection point for the US economy. A break from the long-standing 2–3% growth regime toward a more durable, productivity-led expansion now looks plausible. A 5% GDP quarter within the next year no longer feels far-fetched.

The Dow approaching 50,000 reflects this transition. It speaks less to narrow tech exuberance and more to a broadening rotation into banks, industrials, and consumers. Tech leadership may pause, but the baton is moving through the real economy before cycling back. That rotation does not signal risk aversion. It marks a bull market functioning as it should.

The Next Economy Runs on Compute – and Big Tech Knows It

Over the past three months, markets and geopolitics have been driven by a volatile mix of AI euphoria – and AI fear – alongside fiscal uncertainty and rising geopolitical risk.

Global equities have been repeatedly jolted by one central question: Are Big Tech’s massive AI capital spending plans, laying the foundations for the next productivity boom, or inflating the next capex bubble?

Each new spending announcement has been met with suspicion, with comparisons to the dot-com era drawn reflexively-even when those parallels feel increasingly forced.

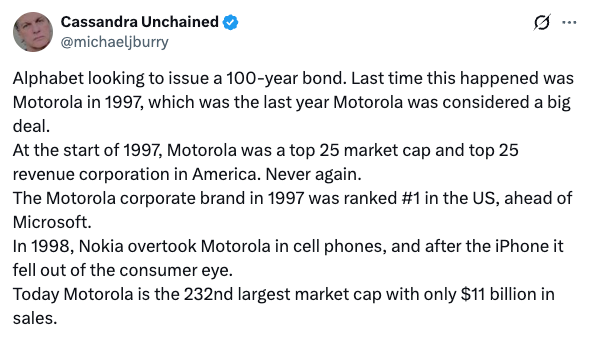

This week’s catalyst came from comments by US investor Michael Burry, responding to Alphabet issuance of a 100-year bond.

Burry warned: “Last time this happened was Motorola in 1997.”

It’s a clever line – -but it rests on an outdated framework. The Motorola comparison says less about Alphabet’s fragility, and more about the limits of applying legacy tech analogies to a compute-driven world.

Source: Michael Burry on X

Motorola in 1997, was a one-product company riding a fading cycle, with no ecosystem, eroding pricing power, and distribution about to be commoditized.

Alphabet today is the inverse. It sits on over $120bn in cash, generates approximately $75bn in annual free cash flow, and saw more than $100bn of demand for a bond deal initially sized at $15bn. Even after expanding long-term debt to approximately $46.5bn, Alphabet’s debt-to-cash ratio remains comfortably below 0.5x.

This isn’t survival financing. It’s infrastructure financing.

The market is missing the bigger point. AI has turned compute into a strategic asset, not a utility. And strategic assets are never about shared access –they’re about control.

Alphabet isn’t issuing century debt because it’s desperate; it’s laying the rails of the next economic system. It could retire a meaningful portion of its debt tomorrow without breaking stride.

This is now a race for compute. Full stop.

The companies that matter most – Microsoft, Amazon, NVIDIA, and Google – won’t just supply compute. They’ll control access, pricing, and deployment speed. When you own the choke point, you own the economics of the ecosystem built on top of it.

This is why the AI capex arms race is accelerating — and why comparisons to past bubbles miss the scale.

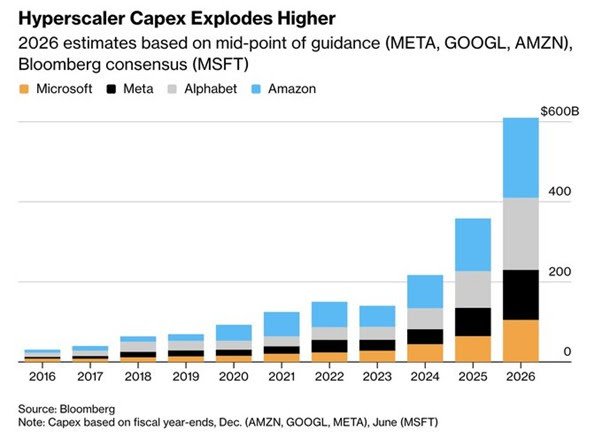

Capex estimates for the Big Four hyperscalers – Microsoft, Meta, Alphabet, and Amazon – have surged to approximately $610bn for 2026, up from $359bn in 2025 (see chart below). That’s not incremental spending. That’s a structural reallocation of capital toward compute, power, and infrastructure.

For context, Bloomberg estimates that 21 of America’s largest industrial companies combined-including automakers, railroads, defence contractors, telecoms, logistics firms, Exxon Mobil, Intel, Walmart, and the companies formerly known as GE-will spend just $180bn on capex in 2026. Big Tech alone is outspending the rest of industrial America by more than 3x.

And before panic sets in, some perspective matters. Hyperscalers are currently reinvesting about 60% of operating cash flow into data centres and capex. Two years ago, that figure was 33%. From 2017–2022, it averaged 27%. Crucially, today’s spending intensity remains well below the 140% of cash flow telecom companies burned through at the peak of the 2001 fibre bubble.

As Brad Gerstner of Altimeter Capital put it: “Think of it as digging a gold mine. You have to spend a lot of money before you get the gold out. These guys are digging the biggest gold mine in the history of software. The real question is whether you believe Andy Jassy, Mark Zuckerberg, Sundar, and Jensen-or think there’s no gold at the bottom.”

That’s the trade. Either this is reckless overbuild-or the upfront cost of controlling the most valuable infrastructure layer of the next economy.

Today, markets obsess over hyperscaler margins and free cash flow. Tomorrow, the focus will be on companies without secured compute access-those renting capacity, inheriting hyperscaler margins, and operating at structurally higher cost.

The cloud worked when compute was cheap. AI has ended that era.

A tech re-rating is underway, but it won’t be uniform. Firms with genuine AI and infrastructure control will benefit disproportionately. Software remains in price discovery. European and emerging-market tech firms without compute ownership face structural de-rating risk. If you sit downstream of someone else’s infrastructure, your margins sit downstream too.

This isn’t about one bond deal-or even one company. It’s about who controls the machines the next economy runs on.

AI turns compute into a strategic weapon. And weapons, historically, are never about shared access.

They’re about control.

Most people are still operating on scarcity logic, in a world that has already moved on.

As those closest to the transformation keep reminding us, including Garry Tan, President & CEO of Y Combinator – what’s unfolding across AI, energy, materials, and biology is a shift from allocation to creation. Yet our political, economic, and cultural systems were built for a different era: Managing scarcity, negotiating slices, deciding who gets what and at whose expense.

They were never designed for exponential technologies that expand the pie faster than institutions can process. When those systems collide with abundance, they don’t recalibrate – they panic.

The failure is as much psychological as it is structural.

If you believe the world is zero-sum, abundance looks like instability. If you believe intelligence, coordination, and technology can scale together, abundance looks like the next stage of civilization.

Markets and the Economy

Before turning to the economy and equities, it’s worth outlining the market structure we are operating in—and likely to remain in for some time.

Markets feel far more volatile than they are- if you listen to headlines instead of price action. Or, to put it more precisely: Markets today are segmented, not contagious.

As Philosopher Heraclitus warned: “Much learning does not teach understanding.” We’re drowning in narratives but missing the signal.

Recent price action makes the point brutally clear. Silver has traded like a meme stock-surging from approximately $40 in September to over $120 in late January, then collapsing back below $65, including two -20% drawdowns in a single week. And yet, during that same stretch, the largest daily move in S&P 500 futures was just –1.2%, while a 9.3basis points (a basis point is 1/100th of a percent) drop in 10-year Treasury yields barely registered against far larger swings seen repeatedly over the past year.

Chaos in selected corners, calm everywhere else.

This disconnect reflects a defining feature of modern markets: Liquidity is everywhere for small positions, but balance-sheet risk is nowhere for big ones.

Years of asset inflation, from equities to housing to crypto, has created a powerful wealth effect, and empowered retail but regulation has stripped institutions of the ability (and incentive) to warehouse risk. The giants that once tied markets together- Dot-com era equity desks, pre-Global Financial Crisis Mortgage-Backed Securities machines- are gone. Price discovery now happens fast, violent, and local.

There are casualties, but they arrive early. As Philosopher Friedrich Nietzsche put it, “What does not kill me makes me stronger.” Rapid price discovery prevents bubbles from metastasizing into systemic threats. Losses are real, but they’re contained-and instructive.

Crypto markets show this most clearly. Heavily leveraged traders are auto-liquidated en masse, clearing positioning in hours, not months. The market goes vertical on the way down-and often rips higher once excess leverage is flushed. Painful? Absolutely. Systemic? No. These losses act as circuit breakers, not accelerants.

Contrast this with the globalization era, when shocks cascaded across borders and balance sheets-from subprime mortgages to sovereign debt crises. Today’s structure does the opposite: it absorbs shocks rather than transmits them.

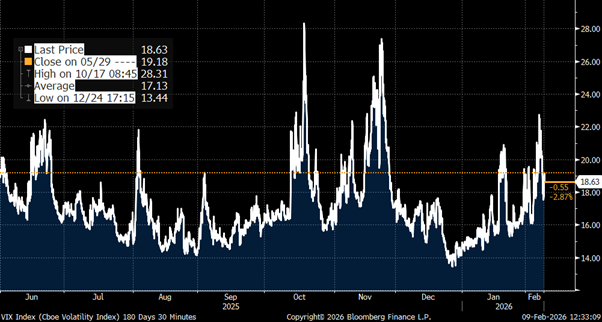

Even volatility itself is telling the story. The VIX has averaged around 17 over the past six months (see chart below), and repeated spikes into the low 20s have failed to spark broader stress-much to the frustration of those still waiting for the long-anticipated equity reckoning.

Conclusion: Volatility is no longer a warning siren- it’s a sanitation mechanism. Big moves don’t signal growing macro danger; they signal risk being cleared. The calm in the S&P 500 amid violent swings elsewhere isn’t complacency-it’s evidence that today’s market system contains risk rather than denying it.

The VIX index – 6-month price chart

Source: Bloomberg

Over a month ago, I wrote a post – “Let’s talk about Kevin” and made a case for why former member of the US Federal Reserve (Fed) Board Kevin Warsh will be the next Fed chair.

Just over a week ago, President Donald Trump formally appointed Kevin Warsh to be the next Chair of the US Fed subject to confirmation hearing by the Senate.

The nomination of Kevin Warsh as Fed Chair has refocused attention on how deeply the Fed is embedded in markets. Warsh has long argued that the Fed’s footprint-still approximately $7.5 trillion-is too large, not just in asset holdings but in blurred lines between monetary and fiscal policy and an overbearing communications regime that shapes investor behaviour.

A Warsh-led Fed is unlikely to change the near-term rate path, but it could gradually shift balance sheet strategy.

Any meaningful shrinkage, however, is constrained by structurally high bank demand for reserves (still above $3 trillion). Move too fast, and funding markets break-something the Fed learned the hard way in 2019.

To understand the direction of travel, it’s worth reading-and re-reading The Wall Street Journal op-ed Warsh co-authored with Stanley Druckenmiller last June: “ The Asset-Rich, Income-Poor Economy ” It offers a clear preview of what may be coming next.

Warsh and Druckenmiller argued – higher asset prices are not translating into meaningful increases in capital expenditures, and the weak growth in business investment is proving to be an opportunity-killer for workers.

Balance-sheet wealth is only durable when it stems from earned economic success rather than government stimulus or financial engineering. True wealth creation requires productive growth – where labour, capital, and innovation raise productivity, converting income into savings, savings into investment, and investment into lasting assets.

Today, the US shows a widening gap between asset-driven balance-sheet gains and income growth that benefits the broader population: many households lack stock ownership or housing wealth, retirees face weak bond returns, and employment recovery has lagged population growth, driving high non-participation.

Meanwhile, corporate incentives favour debt-funded buybacks over long-term investment, rewarding short-term asset inflation instead of productive risk-taking.

The result is rising asset prices alongside subdued ~2% real growth, weak business investment, slower wage gains, and below-trend productivity. Without stronger investment in productive capacity and people, prosperity will remain fragile and uneven – though sweeping deregulation and economy-wide growth initiatives could mark an inflection point toward more durable, productivity-led expansion.

“The Powell Fed has failed to get interest rates about right for most of Chair Powell’s tenure.”

– Kevin Warsh, Oct 12, 2025

“What we need to do is examine the entire Federal Reserve institution and whether it has been successful. All of these PhDs over there-I don’t know what they do. This is like a universal basic income for academic economists.”

– US Treasury Secretary, Scott Bessent, July 21, 2025

Both Bessent and Warsh are aligned on the need for urgent Fed reform. That process is likely to begin as Powell’s term ends on May 15, 2026- or sooner, should he step aside.

A broader agenda of major deregulation, reduced red tape, and growth driven by the full breadth of the US economy-not just Wall Street and tech-could mark a defining inflexion point. If executed well, it may finally lift the US out of its long-running 2–3% GDP growth rut and toward a more durable, productivity-led expansion.

This is something to be really excited about. I will not be surprised if we see +5% GDP growth quarter at some point over the next 12 months.

Bottom line: Fed Chair Warsh wouldn’t pull the Fed out of markets overnight-but he’d push toward a smaller, quieter central bank, slowly and within tight plumbing constraints to engender better GDP growth.

The Dow Jones Industrial Average hit 50,000 for the first time on Friday.

The Dow hitting 50,000 is less about tech euphoria and more about a quiet rotation into the real economy. Over the past six months, the Dow has outperformed both the S&P 500 and the Nasdaq, as investors trimmed crowded AI trades and rotated into banks, industrials, consumer staples, and transport stocks.

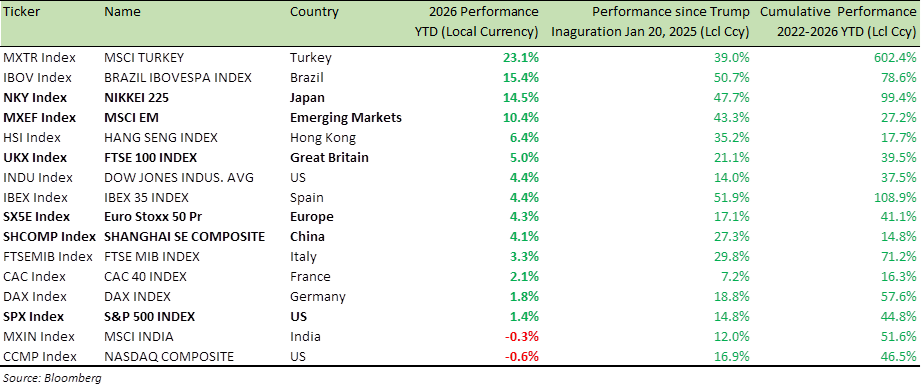

Global Equity Index Performance (2026 YTD, since Jan 20 to YTD and 2022-26 YTD)

While the Nasdaq has been choppy and flat-to-down amid software and AI volatility, and the S&P 500 has delivered modest gains, the Dow has surged-helped by standout performances from names like Walmart, Johnson & Johnson, and Coca-Cola.

At the same time, emerging markets have kept pace or beaten US tech-heavy indices, benefiting from cheaper valuations and a weaker dollar narrative.

The market’s message is clear: this rally isn’t just tech beta-it’s a vote of confidence in reaccelerating US growth, which is good news for both the broader economy and US equities.

Tech may pause and consolidate, but the baton is being passed to the real economy-banks, industrials, transports, and consumer staples-before ultimately rotating back to tech. That handoff, from innovation to picks-and-shovels and back again, isn’t a risk-off signal. It’s a sign of a healthy, durable bull market doing exactly what it’s supposed to do.

A few thoughts on US GDP growth-and yes, try not to laugh.

“If our new head of the Fed [Kevin Warsh] does the job he’s capable of, we can grow at 15%-maybe more.” That was Donald Trump speaking to Fox News on February 9, 2026.

Fifteen percent is…ambitious. I’m not sure the economy-or anyone’s spreadsheets-are ready for that.

Personally, I’d be more than satisfied with +5% real GDP growth, a level the US hasn’t sustained in over two decades, excluding the post-COVID rebound distortions. Even getting close would be meaningful.

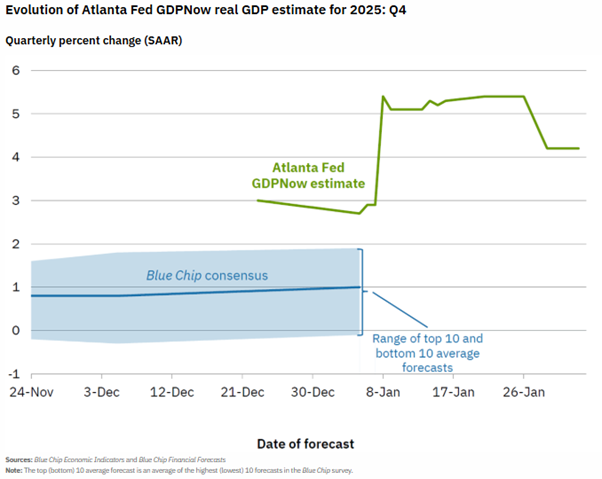

That said, the data are moving in the right direction. The Atlanta Fed’s GDPNow model is tracking +4.2% growth for Q4 2025, putting full-year GDP north of +3%-not fantasy numbers, but strong momentum by modern, post-GFC standards.

US inflation is also behaving better than feared. December CPI rose +0.3% m/m, with headline inflation at +2.7% y/y and core inflation at +2.6%. Importantly, inflation psychology is cooling too: the New York Fed’s consumer survey shows 1-year inflation expectations easing to +3.1%, down from +3.4%.

The US consumer is slowing but not cracking. US Retail sales were flat m/m in December, and core sales dipped -0.1%, pointing to moderation after a strong run rather than outright retrenchment.

Meanwhile, the labour market is cooling in a healthy way. US Payrolls rose 64,000, US unemployment rate sits at 4.6%, and US wage growth remains around 3.5% y/y. Slower hiring alongside steady wages fits a late-cycle but intact expansion-not an economy rolling over.

Bottom line: Growth is solid, inflation is cooling, and the labour market is bending, not breaking.

The journey to S&P 500 at 8,000 and Nasdaq 100 at 30,000 will not be linear. Periodic selloffs and extended sideways phases are inevitable along the way.

That’s precisely where equity structured products come into their own. Used thoughtfully, they are an effective way to navigate-and potentially monetize-higher volatility. These strategies can offer partial capital protection, help define disciplined entry levels, and generate returns even when markets move sideways or pull back.

For tailored ideas, stock-specific structures, or deeper insights, please reach out to me or your dedicated relationship manager.

Best wishes,

Manish Singh, CFA