“When the winds of change blow, some people build walls and others build windmills”

Unknown

Summary

In 1948, as the campaign kicked off, Harry S. Truman’s approval rating had fallen to 36%, and polls had him trailing his opponent Thomas E. Dewey by almost 15 points. On the night of the election, news organizations called the election for Dewey before all votes had been counted. The Chicago Daily Tribune was so sure Dewey would win, that the newspaper brushed off close early returns and printed 150,000 copies of its first edition with the (now) infamous headline “DEWEY DEFEATS TRUMAN.” The morning brought confirmation. Truman had defied the predictions and won the election with 303 electoral votes to Dewey’s 189.

So can President Donald Trump do a Truman and prove the pollsters wrong again as he did in 2016? Has he taken a leaf out President Truman’s 1948 Playbook?

The parallels to the 1948 US elections are striking and while Trump may not admit it, he has in fact taken a leaf out of the Truman playbook. Truman was serene while the pollsters, scribes, Democratic establishment and most of his campaign staff were certain he would meet a crushing defeat on Election Day. The same can be said of Trump and his 2020 campaign. Truman had an unshakable conviction that the issues he had been pushing will lead him to victory and same can be said of Trump. The Trafalgar Group – the only pollster to correctly show Trump with a lead in Michigan and Pennsylvania in 2016 heading into the Election Day- now indicates that Trump is now ahead in Pennsylvania, Florida, Michigan, North Carolina and Biden has a razor-thin lead in Wisconsin. So beware of pollsters and their sweeping predictions. Those who have written off Trump could be in for a rude awakening next Tuesday.

The curious thing is at least on recent evidence, financial markets do not seem to differentiate between a Democrat or a Republican in the White House. Perhaps it’s because the man in the White House at 1600 Pennsylvania Avenue is not in control of the economy as much as the person in the Eccles Building, at 20th Street and Constitution Avenue – the Chairman of the Federal Reserve. It’s all been one big monetary policy-driven market ever since the Great Financial Crisis (GFC) of 2007. Under President Barrack Obama, the three best-performing sectors were Consumer Discretionary, Technology and Healthcare. Under Trump, the three best-performing sectors have been Technology, Consumer Discretionary, and Healthcare. Under Obama, the two worst-performing sectors were Financials followed by Energy. Under Trump, the worst performers were the same.

US election 2020: Will Trump do a Truman?

For weeks and even months now, very few in the mainstream media and political commentariat have had anything positive to say about President Trump and even fewer still consider his re-election a possibility. Some are even predicting that the Democrats will win the White House, the Senate as well as retain control of the House of Representatives. That would be a clean sweep and full control of both the Legislative and the Executive branches of the US government.

Just a few days ago, The Financial Times ran a headline – “US investors pivot to ‘blue wave’ as odds favour Biden.” Those views relied on polls that are showing Trump trailing nationally by double digits, an insurmountable lead.

Yet, these are no ordinary times and pollsters have been consistently wrong in recent times – Trump 2016, Brexit, UK General Elections 2019 to name but a few. If the pollsters get it wrong again, then that may be the end of the “polling industry” as we know it. Pollster Frank Luntz remarked – “If Trump defies polls again, my profession is done. I hate to acknowledge it, because that’s my industry — at least partially — but the public will have no faith. No confidence. Right now, the biggest issue is the trust deficit.”

In 1948, on the eve of the Presidential election, polls had Republican challenger Thomas E. Dewey leading the Democrat President Harry S. Truman by 5-6 points. The New York Times predicted Dewey would get 345 electoral votes and Newsweek predicted 366 votes.

On the night of the election, news organizations called the election for Dewey before all votes had been counted. The Washington correspondent of The Chicago Daily Tribune was so sure Dewey would win, that the newspaper brushed off close early returns and printed 150,000 copies of its first edition with the (now) infamous headline “DEWEY DEFEATS TRUMAN.”

That night, Truman had a glass of milk and went to bed early. Awakened at 4:30 am, he was told he would likely win—and went back to sleep. The morning brought confirmation. Truman had defied the predictions and won the election with 303 electoral votes to Dewey’s 189. He had beaten Dewey by more than 2 million votes and swept all but a handful of farm states and the West.

I love the morning-after photo (see below) of President Truman holding a copy of The Chicago Daily Tribune and beaming. It made for a great picture and one of the most famous political photographs in American history. Dewey went to bed as President-Elect and woke up the loser and, today, very few other than political anorak know of Dewey.

On November 2, 1948, President Truman pokes fun at the expense of his least favourite newspaper, Chicago Daily Tribune

Source: Truman Library Institute

So can Trump do a Truman and prove the pollsters wrong again as he did in 2016? Has he taken a leaf out President Truman’s 1948 Playbook?

The parallels to the 1948 US elections are striking and while Trump may not admit it, he has in fact taken a leaf out of the Truman playbook.

In 1948, a month before the election, nine out of 10 US newspapers (including The New York Times) endorsed Dewey. Certain of a Dewey landslide, one pollster even stopped polling by September. The influential Newsweek magazine took a poll of 50 political writers about the likely outcome of the 1948 election. When the issue appeared, Clark Clifford, then an aide to Harry

Truman, tried to hide the copy under his coat. Truman discovered the magazine, saw that all 50 pundits were predicting Thomas E. Dewey to be the winner, and said, “I know every one of these 50 fellows. There isn’t one of them has enough sense to pound sand in a rat hole.” There’s no love lost between Trump and the US mainstream media as you will know and “fake news” is the most polite of disdain that Trump has for them.

As the campaign kicked off, Truman’s approval rating had fallen to 36%, and polls had him trailing Dewey by almost 15 points. Trump has suffered a similar fate.

Truman was serene while the pollsters, scribes, Democratic establishment and most of his campaign staff were certain he would meet a crushing defeat on Election Day. The same can be said of Trump and his 2020 campaign.

Truman had an unshakable conviction that the issues he had been pushing and would push—affordable health insurance for all, raising the minimum wage, aid to education, civil rights, resistance to Stalinist Russia and storage for farmers’ surplus crops—would trump Dewey’s a low-risk campaign. Similarly, Trump has pursued and campaigned on policies that he thinks poll well with the people and will get him elected – tax cuts, law and order, China, energy/fracking and the Supreme Court to name a few. In contrast, Biden has run a low-risk campaign hoping to keep his lead, “play safe” and sail into the White House. Biden’s leisurely campaign in car parks resembles more a coffee shop talk. Trump’s campaign is frenetic and resembles an actual political rally dwelling on differences with his rival.

Truman had a revolutionary campaign plan – he would tirelessly crisscross the country from Labour Day to election eve in his private railroad car, the ornate Ferdinand Magellan, talking unscripted to voters from dawn to midnight. Trump is doing the same. He is campaigning with full ferocity just like Truman did in 1948. Fresh off recovering from coronavirus, Trump has scaled the length and breadth of the country displaying energy and vitality in doing as many as three rallies a day. Trump has upped the ante last few days by highlighting Biden’s flip-flop and controversial statements by playing videos of them on a giant screen at his rallies. Trump dances off stage to the Village People’s “YMCA” as the rallies wrap up. You just have to see his campaign and listen to his speeches to see the reception he gets compared to Biden.

A Trump rally in progress

Source: votedonaldtrump.com

In 2016, Robert Cahaly, senior strategist for the Trafalgar Group, made a name for himself by being the only pollster to correctly show Donald Trump with a lead in Michigan and Pennsylvania – two key states he carried – heading into the Election Day. In 2018, Cahaly’s method once again proved solid. In one of the most polled races of the cycle, Trafalgar stood alone as the only polling firm to correctly show a Ron DeSantis gubernatorial victory in Florida – as well as Rick Scott winning the Senate race there.

So what does Trafalgar say now?

In the key battleground of Pennsylvania, the Trafalgar polls have moved in favour of Trump over the last four weeks. On Tuesday, Trafalgar group indicated that President Trump is now ahead in Pennsylvania (Trump 48.4, Biden 47.6). This same poll had Biden 3 points ahead a month ago and 6 points ahead in July/August. Trafalgar poll also indicates President Trump is ahead in Florida, Michigan, North Carolina and Biden has a razor-thin lead in Wisconsin.

So beware of pollsters and their sweeping predictions. Those who have written off Trump could be in for a rude awakening next Tuesday.

Markets and the Economy

Investors spend so much time analysing US elections. Is it worth it?

Yes, there’s a difference in style and substance between the candidates but what does the outcome mean for risk assets?

The curious thing is at least on recent evidence, financial markets do not seem to differentiate between a Democrat or a Republican in the White House. Perhaps it’s because the man in the White House at 1600 Pennsylvania Avenue is not in control of the economy as much as the person in the Eccles Building, 20th Street and Constitution Avenue – the Chairman of the Federal Reserve. It’s all been one big monetary policy-driven market ever since the Great Financial Crisis (GFC) of 2007.

Numbers crunched by our research providers Gavekal Research indicate:

- Equities, as measured by the S&P 500, delivered roughly the same return during the President Barrack Obama years as under Trump: +12.38% annualized for Obama and +13.87% for Trump.

- Long-dated bonds delivered positive returns in the Obama years of +6.85%, and even better positive returns in the Trump years of +9.85%

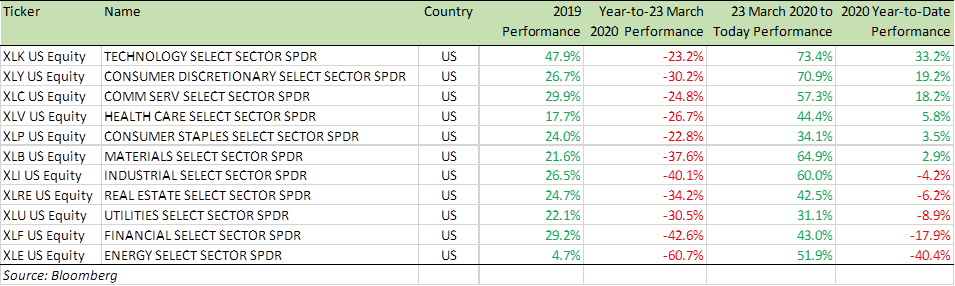

- Under Obama, the three best-performing sectors were Consumer Discretionary, Technology and Healthcare. Under Trump, the three best-performing sectors have been Technology, followed by Consumer Discretionary, and then Healthcare (charts above)

- Under Obama, the two worst-performing sectors were Financials followed by Energy. Under Trump, the worst performers were the same

- Trump’s promises to “make America great again,” bring manufacturing jobs home, and impose tariffs on China etc., didn’t do any good for the Industrials sector. Industrials finished in sixth place, just as they did under Obama

- Trump years were all about deregulation yet the financial sector returns did not get a boost. Financials finished second to last again as under Obama. Fed’s zero-rate policy and flattening the yield curve, sucked the life out of financial earnings

- Energy returns were bad in the Obama years, known for stringent regulations and climate change curbs, but at least they were positive. In the Trump years, we saw regulatory burdens slashed and Trump pulling the US out of the Paris Accord, yet Energy was the only sector to deliver negative returns

What it means is that the structural and market forces are much more powerful and long-lasting once they take shape. A country’s political leadership may think it has control, but it may not despite its best intentions and efforts.

My recommendation is to focus on large secular trends: The big wave and not to get lost in the ripples which can be exciting and you may think you have figured everything – out only to be swept away when the big wave arrives.

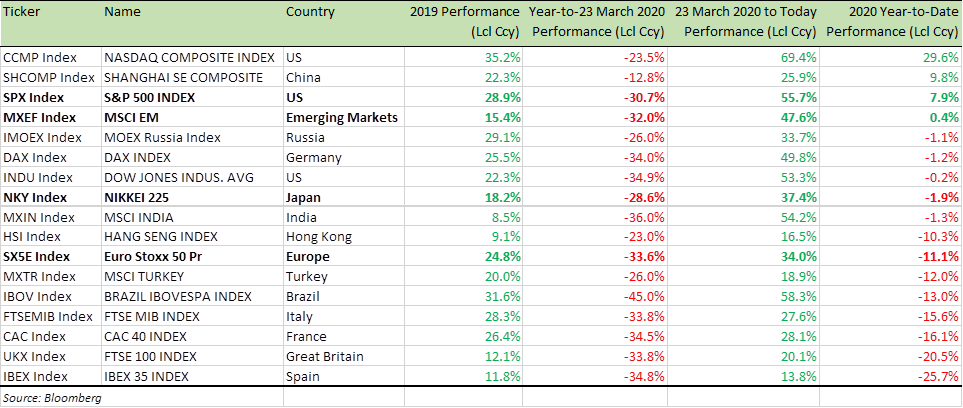

Benchmark Equity Index Performance (2019 & YTD)

The big trend of tech stocks and China stocks doing well has continued as the table above indicates and it has more legs to go, especially the latter as Europe and the US still struggle with controlling Covid-19.

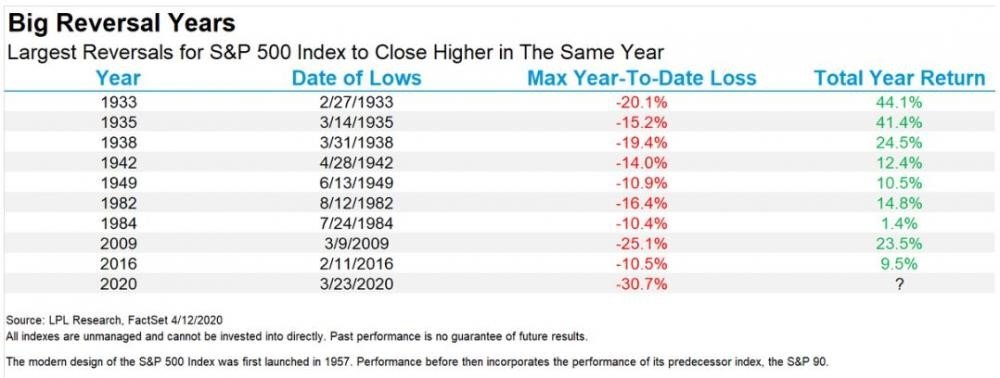

In last month’s Market Viewpoints, I warned: “of a volatile 4-6 weeks period ahead, as we see the pre and post-US election events play out”. With the elections less than a week away, we are truly in the midst of a volatile period which has seen the S&P 500 suffer a -8% sell-off from its mid-October highs. I, however, continue to be bullish on equities and see the sell-off as an opportunity to “buy the dip.” My favourite sectors to pick stocks from –Consumer Staple (XLP) and Consumer Discretionary (XLY) as well as Tech (XLK) and Communications (XLC)

Benchmark US equity sector performance (2019 & YTD)

In Europe, it’s batten down the hatches time as France and Germany announced new lockdowns last night. A national lockdown, which will begin Friday and last at least one month, will require the French people to remain inside their homes while restaurants, bars and shops, deemed nonessential, will close. German Chancellor Angela Merkel said the country’s Federal and State governments had agreed to a one-month shutdown of restaurants, bars, fitness studios, concert halls and theatres, starting November 2. Hotels are barred from hosting tourists until the end of November, she said, and public gatherings will be limited to 10 people from two households and schools will remain open. Tough measures but not a complete lockdown.

The virus spread we are seeing now in Europe was the spread that didn’t happen in May-June because Europe imposed a complete lockdown. Lockdowns are an easy approach, but it will not help prevent the spread of the virus. Without a vaccine or wide enough immunity, every time lockdown is lifted the spread will increase, as we are seeing now. We will have to shield the most vulnerable, take all precautions and live with the virus until a vaccine is found.

The restrictions from Eurozone’s two biggest economies – Germany and France are not good news for the Eurostoxx 50 (SX5E) Index. However, I see this as an opportunity to start building long positions in SX5E. Every iteration of the lockdown will be less severe as economic costs add up rapidly. The re-opening therefore will continue. Besides, governments are compensating businesses and workers for lost earning, s so consumer spending is unlikely to take a big hit.

As the charts above show, Germany and France have borrowed lavishly relative to the size of the GDP downturns they are forecast to sustain this year. Meanwhile, Italy and Spain, which the European Commission forecasts will suffer deeper downturns, have borrowed less relative to the depths of their slumps. The roll-out next year of disbursements from the EU’s planned recovery fund will help offset some of the pain for Italy and Spain.

For specific stock recommendations, please do not hesitate to get in touch.

Best wishes,

Manish Singh, CFA

")