“Europe is at a crossroads and must embrace reform to revitalize its economic prospects and Making Europe Great Again (MEGA)”

Summary

In his address to the UN General Assembly in September 2018, President Donald Trump cautioned that Germany could become heavily dependent on Russian energy if it didn’t alter its course. This remark, met with derisive smirks from the German delegation including Foreign Minister Heiko Maas, has proven prophetic as Germany now teeters on the edge of a third year of recession. After two years of downturn, Germany’s hopes for a post-COVID recovery have vanished, with manufacturing output dropping 10% and rising energy costs and declining exports leading to significant job losses.

Trump’s stance on reciprocal tariffs, insistence on NATO members contributing their fair share, and his “America First” policy have underscored the theme of “Europe Alone,” prompting a re-evaluation of economic policies across Europe. Germany’s economic slowdown is largely due to self-imposed factors such as an aging workforce, rigid labour laws, and excessive regulations which hamper growth and competitiveness. These challenges are the result of domestic policy decisions rather than the US.

However, there’s a silver lining: these self-inflicted issues present an opportunity for change and improvement. Europe is at a crossroads and must embrace reform to revitalize its economic prospects. The call for “Making Europe Great Again” (MEGA) resonates with the proposed solutions by Germany’s likely next Chancellor, Merz, who advocates for extensive corporate and income tax reductions, the construction of new power stations to lower some of the world’s highest electricity costs, and swift economic deregulation. Concurrently, the SPD aims to boost government investment in infrastructure and military enhancements.

Meanwhile, Trump and US Treasury Secretary Scott Bessent are focused on reducing and stabilizing US Treasury yields, weakening the US dollar, and cutting oil prices to stimulate the American economy. While bond yields and oil prices have reacted positively, the US dollar remains strong. Trump’s policies are poised to bolster both the US economy and its stock market in the foreseeable future, suggesting a strategic advantage in staying overweight US equities.

Is MAGA Becoming Too Much? Time to Shift the Focus to MEGA?

President Donald Trump, reflecting on his first term, has likely adapted his strategy from merely responding to and refuting media claims about his statements and intentions. Now, he is taking a more proactive approach, bombarding the media—and indeed everyone—with a relentless stream of daily announcements. This tactic aligns with what former White House Chief Strategist Steve Bannon has termed, a “day of thunder” approach to media management.

Trump is banking on the idea that the media can only focus on one issue at a time.

By relentlessly flooding the news cycle, his administration keeps the press overwhelmed, leaving little room to shape a coherent narrative—let alone craft a credible response to each announcement.

One day it’s the Department of Government Efficiency (DOGE), the next it’s tariffs on, then tariffs delayed. China deal, China no deal. Europe bad, Europe good. Canada tariff, Canada 51st state, Gulf of Mexico renamed. Federal employees fired, sackings at the Department of Defence and Department of Justice. USAID defunded; contracts cancelled. Zelensky is a dictator, Russia didn’t start the war, we need Ukraine’s mineral rights. Peace deal with Russia, ceasefire now, vote alongside Russia at the UN.

And so, it goes—chaos by design.

Trump backed Elon Musk’s demand that federal employees explain their recent accomplishments by the end of week or risk getting fired, even as government agency officials were told that compliance with Musk’s edict was voluntary.

So, what’s next?

Trump holds press conferences almost every other day, commanding the spotlight from the Oval Office, like a seasoned pro. One moment he’s scolding reporters, the next he’s cracking jokes—turning what starts as a 30-minute briefing into a 90-minute spectacle.

We are not even two months into his 4-year term. So, if you’ve had enough of MAGA, maybe it’s time to focus on MEGA – Make Europe Great Again?

Navigating Troubled Waters: Europe’s Quest for Economic Sovereignty

Trump’s policies— reciprocal tariffs on trade partners, demanding that NATO nations pay their fair share and “America First”—are forcing Europe to confront the reality of “Europe Alone.”

But Europe has no one to blame but itself. European Union (EU) leaders have long talked about strengthening the bloc and making grand promises of reform.

Yet, like a procrastinating student, they’ve pushed the hard work aside, always postponing it to another day.

Well, that day has arrived. The homework is due, and there’s no more time to delay.

Remember this image from September 2018 (see photo below)?

It belongs in The Louvre or The Smithsonian museums: “German delegation laughs after Trump warns of reliance on foreign oil.”

German delegation at the United Nations, September 2018

Source: Bloomberg

The context:

“Germany will become totally dependent on Russian energy if it does not immediately change course,” Trump warned during his UN Speech.

The German delegation, caught on camera, smirked in response. That wasn’t nervous laughter—it was outright scorn. How wrong they’ve been proven, and Germany is about to enter its third year of recession as its manufacturing prowess strains under the cost of high energy prices and competition from China.

Renowned German columnist Wolfgang Münchau, author of Kaput—The End of the German Miracle, put it bluntly:

“The problem with consensus societies is that sometimes the consensus is wrong, and when it is, there is no corrective mechanism. It’s the opposite of a whistleblower society.”

He was speaking about Germany, but it applies to Europe as a whole.

Europe needs decisive leadership, not the hesitation and indecision that defined former Chancellor’s Angela Merkel’s tenure—failures that led to the “immigration crisis” and fuelled the rise of far-right Alternative for Germany (AfD), in Germany.

Robin Alexander, deputy editor of Die Welt, details this in his 2017 book Die Getriebenen (The Driven) – the biggest influx of people in postwar German history, wasn’t the result of a bold decision, but rather the absence of one.

“The border stayed open, not because Merkel deliberately decided so, nor anyone else in the federal government,” Alexander writes. “At the crucial moment, there was simply no one willing to take responsibility for closing it.”

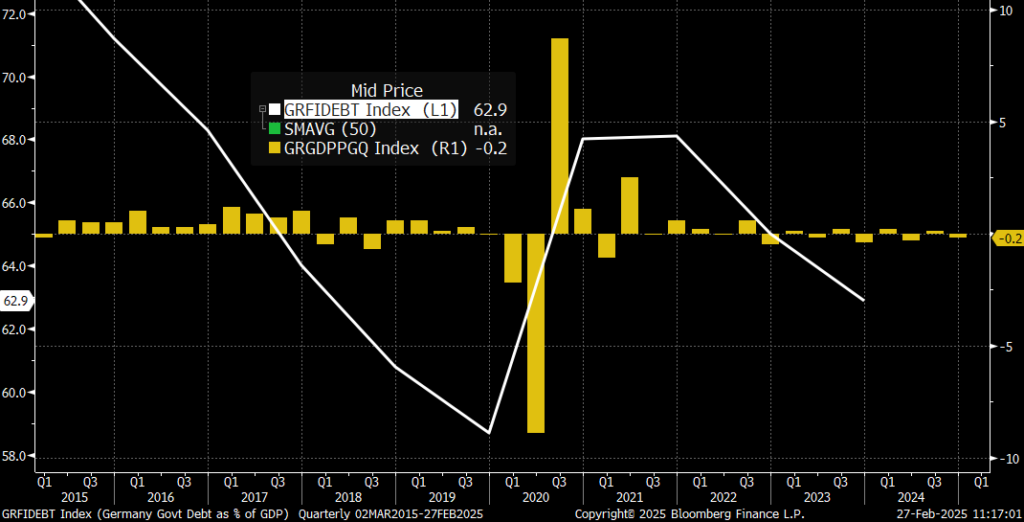

Europe’s former growth engine, Germany has shrunk for two years in a row (see chart below), erasing any recovery made sense the Covid-19 pandemic. Its manufacturing output is down about -10% over the same period and its companies, squeezed between rising energy costs and falling exports, are shedding thousands of jobs a month.

5-year chart: Germany debt as % of GDP (white line) and Germany QoQ GDP growth as % (yellow bars)

Source: Bloomberg

Very soon Germany will have a new Chancellor and it’s likely going to be the CDU/CSU candidate Fredrich Merz. If Merz fails to solve Germany’s growth, migration, and economic issue then the AfD, could be in office in four years’ time or before.

Besides the national issues of EU nations, at the European level, if MEGA is to be a success, then some fundamental changes must take place. Here’s one reminder from a recent speech by Mario Draghi, former Italian Prime Minister, and former President of the European Central Bank (ECB)

“The IMF estimates that Europe’s internal barriers are equivalent to a tariff of 45% for manufacturing and 110% for services.”

Europe is an ageing, debt-ridden continent, struggling with stagnation and unable to defend itself without US assistance. To make matters worse, the global order—trade, borders, defence, and technology—is being rewritten. Now, this can be threat or an opportunity. I hope it’s the latter.

Europe will need to reduce welfare spending (with the region making up 7% of the world’s population, 25% of global GDP, but accounting for 50% of social spending), boost defence spending, and work towards unifying its capital markets, as Draghi has emphasized. It will also need to deregulate and create a more business-friendly environment, strengthen ties with the UK, and challenge the bureaucratic barriers that hinder growth and entrepreneurship.

There is hope!

Germany’s incoming chancellor, Merz, has called for sweeping corporate and income tax cuts, building 50 new power stations to bring some of the world’s highest electricity prices down, and for the rapid deregulation of the economy.

The SPD, meanwhile, wants to unleash government investments to help fix Germany’s decrepit infrastructure and prop up its military.

On the US, Merz’s remark was very eyebrow raising. He said – “It is clear that the Americans—at least this administration—are largely indifferent to the fate of Europe,” he declared. He then made his stance clear: his “absolute priority” is to help Europe achieve “independence from the USA.”

Reality is very different.

None of the challenges Merz faces within Germany, seem to stem from US actions.

Take the energy crisis, for instance—this was largely the result of Germany’s own push for renewable energy (Energiewende) and the premature closure of nuclear power plants, policies driven by the country’s green agenda. This choice made Germany heavily reliant on Russian natural gas, which backfired when tensions with Russia escalated.

Germany’s productivity and labour challenges are also self-inflicted. A rapidly aging workforce, inflexible labour laws, and an overregulated economy have all slowed economic growth and raised concerns about competitiveness. None of this was imposed by the US, no matter what the Trump haters in Germany (and Europe) would like to say.

While some comments from American politicians may seem harsh, the truth is that Germany—like much of Europe—is dealing with the consequences of its own policy decisions.

There’s a silver lining: Self-inflicted problems require one to change and make amends. Europe must seize the moment and get working on Making Europe Great Again (MEGA).

Markets and the Economy

The S&P 500 (SPX) is back to early November levels, when Trump won the US election. The euphoria has given way to inflation and trade war fears, as Trump continues to issue executive orders like confetti.

Now, I don’t mean to be bearish. There’s always something to worry about in the market—that’s nothing new. Uncertainty feels more pressing, when too many pieces are moving – fiscal, monetary, political, international and trade security, and geopolitics.

Global Equity Index Performance (2025 YTD, 2022-2025 YTD and 2024 Performance)

Analysing the recent news flow, reveals several concerning economic indicators:

- Despite the SPX reaching new highs, its cumulative advance/decline (A/D) line has not kept pace, indicating a negative divergence.

- The U.S. housing market remains sluggish—high mortgage rates continue to suppress demand, and conditions have not shown improvement even after the Federal Reserve began cutting rates in September. With the spring selling season on the horizon, prospects for recovery appear limited.

- Inflation remains a pressing issue. Recent CPI and PPI reports have demonstrated price pressures exceeding expectations, with significant spikes in the Prices Paid and Prices Received components of the New York and Philadelphia Fed surveys.

- Although the earnings season has generally been positive, corporate outlooks are trending negative, with twice as many companies revising their forecasts downward as those reporting optimistic projections.

On the brighter side though:

- The 10-year Treasury yield has dropped significantly since the latest CPI report and is currently at +4.3% far cry from fears of +5% couple of months ago, suggesting the market isn’t pricing in another inflation surge.

- Sector breadth has also been strong. Seven of the eleven S&P 500 sectors are outperforming the index by over +4%—a historically strong indicator of market resilience.

- Additionally, since the January lows, the market has seen consistent buying on weakness (Friday being an exception). Over the last five weeks, the S&P 500 SPDR ETF (SPY) closed higher than it opened on 18 of 25 trading days—the highest rate since late 2023. That signals accumulation and investor confidence.

Benchmark US equity sector performance (2022-2025 YTD, 2023-24, 2025 YTD, and 2025 YTD relative to the S&P 500 Index)

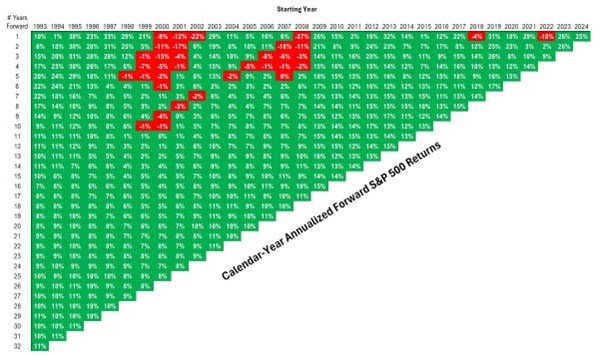

Take a look at this insightful chart from Ben Carlson’s A Wealth of Common Sense blog, showcasing the SPX annual returns since 1993.

As you can see, there are significantly more green (gains) than red (losses), highlighting a key takeaway—despite the market upheavals of the past 30 years, patience and a medium-term investment approach have consistently outperformed short-term trading strategies.

How to read the chart: Select a starting year and follow the timeline downward to see the corresponding annualised return.

For example, a nine-year investment beginning in 1993 would have delivered a 14% annual return. The chart reveals more green (gains) than red (losses) over the years, though investors have certainly faced some tough stretches along the way.

A historical analysis of SPX returns since 1993 highlights the power of long-term investing.

- Long-Term Wins: Holding for 11+ years never resulted in losses, while shorter periods (2-5 years) saw multiple downturns.

- Return Ranges:

- 10-year annual returns varied from -1% to 17%.

- 15-year returns ranged from 4% to 14%.

- 5-year returns spanned -2% to 29%.

- Consistency Over Time: Despite major crises—including the dot-com bubble, 9/11, the Great Financial Crisis, and the pandemic—the market still averaged a 10% annual return over 31 years.

- Key Takeaway: While market timing affects short-term results, a long-term approach smooths out volatility and remains the best investment strategy.

S&P 500 annualised gains grid 1993-2024

Source: Ben Carlson, A Wealth of Common-Sense blog

Trump and US Treasury Secretary Scott Bessent have three main goals: Drive down and stabilize US Treasury yields, weaken the US dollar, and lower oil prices—all aimed at fuelling a US economic boom.

Bond yields have responded and so have oil prices, the US dollar is unlikely to for now.

Trump’s policies are set to benefit the US economy and stock market—both in the short term and over the long haul. Staying overweight US equities remains the trade.

Here’s why:

What DOGE is doing in the US may look a bit erratic sometime but cutting spending, lowering deficit is the path that the US is on.

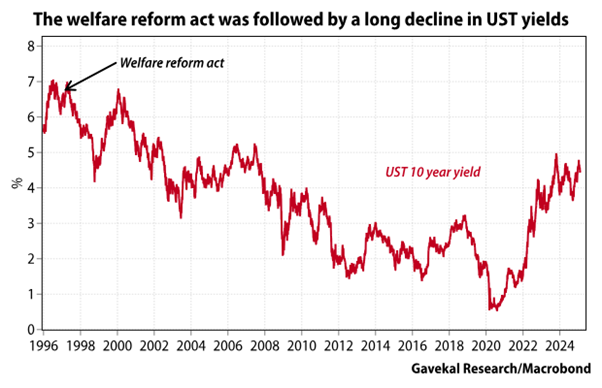

There’s a precedent to it.

In August 1996, then President Bill Clinton signed the Republican-backed Welfare Reform Act, officially known as the Personal Responsibility and Work Opportunity Reconciliation Act (PRWORA), which reduced US public welfare payments.

At the time, US Treasury yields were nearly +7%, a level they would never reach again. Critics feared the worst. Defenders of the status quo were alarmed that lawmakers had not only imposed a work requirement on recipients, but restricted welfare benefits to five years.

“We know how welfare reform will turn out,” warned an article in the New Republic after Clinton signed the Act. “Wages will go down, families will fracture, millions of children will be more miserable than ever.”

- Between August 1996 and September 2000, the number of families on welfare declined by 50%. Welfare caseloads dropped substantially, from 5.5% of the total US population in 1994 to 2.1% in June 2001

- Prior to the Act’s passage in 1996, there were 12.6 million Americans enrolled in the nation’s welfare program. Two decades later, only 2.8 million remained in welfare. Many former welfare recipients entered the workforce, and poverty among children overall fell from 1993 to 1999

While several factors contributed to this shift, including the surge in tax revenue from the dot-com boom in 1996-99, the Welfare Reform Act did achieve its intended goal.

A similar outcome could improve the US fiscal and budget situation this time around. Many people believe that reducing government spending and achieving greater efficiency is nearly impossible. A prime example is the UK’s National Health Service (NHS), where budget allocations keep increasing, yet longer delays in patient care remain the result. We’ve grown accustomed to expecting continued government spending.

However, it’s likely that the world, particularly Europe, will soon learn how spending cuts, better allocation, and greater efficiency can be accomplished.

On an external front, the US is looking to make more savings (and increase revenue).

Trump and Vice President Vance have effectively declared NATO obsolete, asserting that the US will no longer solely fund Europe’s security. This situation forces European countries, especially Poland, Germany, and the Baltic states, to consider two main options:

- Strengthen ties with the US – Increase defence spending, purchase more American-made military equipment like F-35s and missile systems, and maintain favourable relations with Trump.

- Seek a new understanding with Russia – If US-Russia relations improve under Trump, Eastern Europe might recalibrate its approach, perceiving Moscow as a reduced threat.

Regardless of the perceived threat from Russia, European nations must maintain strong relations with the US. Ultimately, Washington holds the essential military and geopolitical power to ensure Europe’s security..

The stock market is unique, in that people often flee during a “sale” rather than capitalize on it. Investors flock to buy when prices are high, fearing they’ll miss out on the gains others are achieving. Yet, paradoxically, they hesitate to purchase when prices drop, only to buy back in when prices climb again.

It’s essential to become comfortable with market downturns.

Embrace the “bear” market.

Make friends with the “bear.”

You can learn a lot from “bears.”

As legendary investor Warren Buffett once said – “If a stock [I own] goes down 50%, I’d look forward to it. In fact, I would offer you a significant sum of money if you could give me the opportunity for all of my stocks to go down 50% over the next month.”

If you own quality stocks, you should hope for prices to drop, not rise—that way, you can buy even more at a discount before they rebound. It’s just common sense.

The key? Good stocks.

For specific stock recommendations and insights related to structured products, please do not hesitate to reach out to me, or to your dedicated relationship manager.

Best wishes,

Manish Singh, CFA