Extreme outcomes are easy to imagine and often dominate attention in uncertain times—but they rarely fully materialize.

Summary

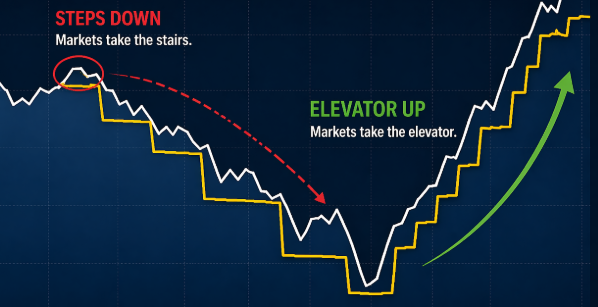

The S&P 500 move since late February may be one of the clearest recent examples of a pattern inversion: Stairs down, elevator up. From the lows triggered by the Iran conflict, the index has now recovered to a fresh all-time high.

The biggest risk in this environment is not the market itself. It is the reaction to it. You do not need to predict volatility to build wealth. You need the discipline to stay invested through it. Every cycle carries its own narrative; the behavioural errors tend to be identical across all of them. Investors reprice fear too aggressively, exit at the wrong moment, and return too late.

What investors consistently get wrong is not the event, but the reaction function. The tendency is to focus on what should happen: markets should fall further, risks should be repriced more aggressively, geopolitics should matter for longer. But “should” reflects bias, not probability. Markets price the distribution of outcomes, not the most emotionally compelling one. Extreme scenarios dominate attention in periods of elevated uncertainty. They rarely play out in full. Meanwhile, the market adapts, discounts, and moves forward even when the underlying situation remains unresolved.

The recovery in equities has been notable, but not excessive.

Despite rallying more than +11% from recent lows, the S&P 500 is up only around +3% year-to-date. The NASDAQ has outperformed, rising approximately +17% from the lows and around +4% on the year. What stands out is the absence of positioning excess. A classic FOMO phase, characterised by aggressive inflows and broad retail participation, has not materialised. If geopolitical risk continues to fade and earnings hold, that phase may still be ahead of us.

Markets don’t wait for peace. They just move on

One year on from “Liberation Day,” the lesson remains as relevant as ever: Markets react violently to shocks – but they don’t stay there for long.

When President Donald Trump stepped into the Rose Garden on April 2 last year, the S&P 500 was already under pressure. Investors expected tariffs and expected near-term pain, but they also believed it would be manageable. The index closed less than -2% down that day, reflecting a consensus that the risk was understood and largely priced in. Within 48 hours, that assumption was shattered. The S&P 500 fell roughly -10%, not because tariffs were introduced, but because they were far more aggressive than anticipated. It wasn’t the event itself – it was the gap between expectation and reality.

Fast forward to today, and the parallels are striking.

In late February, if you had asked investors to model a scenario where the US and Israel attack Iran, retaliation spreads across the Gulf, drones and missiles strike major regional players, and the Strait of Hormuz effectively shuts down – collapsing ship traffic from around 130 vessels a day to single digits -the overwhelming consensus would have been clear. Equities would be down 20–30%, with a prolonged recovery ahead.

That’s not what happened.

S&P 500 and start of the Iran conflict (27/02)

Source: Bloomberg

The actual drawdown in the S&P 500 was closer to -9%, at its worst. Seven weeks on, the market is at a new all-time high. This is even though the conflict remains unresolved, tensions are still elevated, and oil prices have moved meaningfully higher.

This is the uncomfortable truth about markets: They don’t wait for clarity, and they certainly don’t wait for resolution. They reprice quickly, adjust positioning, and move on. The initial reaction is driven by fear and uncertainty, but once the worst-case scenarios are partially discounted and not immediately realised, markets stabilise far faster than expected.

We’re all familiar with the saying that markets “take the stairs up and the elevator down.” This time, it’s been the reverse (see chart above). As market structure evolves, so do the patterns. This may well be one of the clearest examples yet of stairs down, elevator up, with the S&P 500 now back at a fresh all-time high.

The biggest risk today isn’t the market; it’s how one reacts to it.

You don’t need to predict volatility; to create wealth, you need to have the behavioural resilience to survive it.

Every cycle feels unique, every risk feels unique and different, more often than not, the behavioural mistakes many make are the same old – reprice fear way too high, abandon and come back too late.

Don’t get scared out of your trades.

What investors consistently get wrong is not the event itself, but the reaction function. There is a tendency to focus on what should happen – markets should fall further, risks should be repriced more aggressively, geopolitics should matter for longer. But “should” is simply a reflection of bias. Markets don’t reward that. They price probabilities, not opinions.

Extreme outcomes are easy to imagine and tend to dominate attention, particularly in periods of heightened uncertainty. But they rarely play out in full. Meanwhile, the market is constantly adapting, discounting a range of outcomes and moving forward even as the underlying situation remains unresolved.

The implication is straightforward. If you remain fearful for longer than the market does, you are likely to miss the recovery. The objective is not to predict every shock, but to construct portfolios that can withstand them—protecting downside without sacrificing participation in the upside.

Different backdrop. Same conclusion.

Markets don’t wait for peace. They just move on.

Schrödinger Strait

In the thought experiment proposed by Erwin Schrödinger, the renowned physicist, a cat confined in a box is both alive and dead until the box it’s in is opened – a provocation meant to illustrate the peculiar logic of quantum mechanics. Applied, loosely to today’s maritime tensions in the Strait of Hormuz, the idea captures a disquieting truth: The Strait of Hormuz is at once open and closed.

Formally, if you believe both the US and Iran, the Strait has been restored to normal traffic. In practice, however, the picture is murkier.

Risk premia rise and fall with each incident. Tankers carrying oil and gas adjust routes, and schedules. Insurers recalibrate exposure and recalculate premiums.

Naval escorts (or blockades) become more visible. None of this amount to closure. Yet neither does it resemble normality.

The Strait exists in a condition akin to Schrödinger’s cat: Open in law, constrained in behaviour.

That said, such ambiguity is not accidental; it is instrumental.

For Iran the ability to unsettle the Strait without crossing the threshold of outright disruption, offers leverage at a tolerable cost.

For the US, the imperative is to deter escalation without overcommitting.

The result is a managed instability – volatile enough to command attention, contained enough to avoid catastrophe, “harmless” enough to give risk assets a relief and boost like we have seen over the last ten days.

Iran conflict and the region around the Strait of Hormuz

As one would imagine, the economic consequences are subtle but significant.

Energy markets price in probability rather than fact. Insurance costs, freight rates and hedging strategies all reflect a spectrum of possible outcomes, not a settled state. In effect, the strait’s uncertainty becomes a tax on global trade the longer it continues.

So far the market seems to think or at least believe a resolution is in sight. What it may get is another extension of ceasefire and not a final deal.

I was on CNBC earlier this week and as I said on the show, the present situation in the Strait is a ceasefire, not a solution. I do not expect a deal, I don’t think anyone does.

We will likely see an extension of the ceasefire.

For now, the Strait of Hormuz remains navigable. But it is no longer straightforward. Like Schrödinger’s cat, its status depends on perspective – simultaneously open and closed, stable and fragile.

The world may continue to trade through it. Yet it does so in a state of suspended certainty, where perception carries as much weight as reality.

As for President Trump and his recent posts and public statements, in my view he has lost a notable degree of support both at home and abroad since the conflict began. His tendency to alternate between provocative rhetoric and more conciliatory messaging, particularly on social media, doesn’t convey calculated unpredictability. Rather, it gives the impression of reactivity and uncertainty. From a strategic perspective, that’s a vulnerability others can exploit. A leader who changes tone frequently, reacts emotionally to unfolding events rather than shaping them, and resists informed counsel is unlikely to force meaningful concessions. More often, such a leader can be outmanoeuvred and outlasted.

Iran, for its part, doesn’t appear intimidated. If anything, it seems to have assessed the situation carefully and adapted. Leaders who respond to every news cycle are easier to read, easier to influence, and easier to wear down in negotiations. A deal will likely emerge—Iran has clear incentives, particularly around oil exports—but it may not be on the stringent terms Trump sought.

We can all rejoice when this is over, and S&P 500 scales to 8,000.

Markets and the Economy

Kevin Warsh’s confirmation hearing to lead the US Federal Reserve (Fed) began this week, before the Senate Banking Committee and while the nomination has cleared procedural hurdles, the path to full confirmation remains finely balanced.

The constraint is not ideological, but arithmetic. Republicans hold a narrow 13–11 majority on the Committee. However, Senator Thom Tillis (R-NC), has indicated he will block the nomination pending the resolution of a federal probe into outgoing Fed Chair Jerome Powell. Should Tillis join all 11 Democrats in opposition, the vote would deadlock at 12–12, effectively halting the nomination. Warsh advances only if Tillis abstains or votes “present” – a precarious position for a nominee expected to unify his own party.

Democrats, for their part, have shown little appetite to provide a path forward. Senator Elizabeth Warren (D-MA), has raised fresh concerns regarding Warsh’s ethics disclosures, particularly around potential conflicts of interest. His personal wealth – estimated between $131 million and $209 million – makes him the wealthiest nominee in Federal Reserve history, with holdings spanning private assets such as SpaceX, prediction markets like Polymarket, and cryptocurrencies. The optics alone ensure scrutiny will remain elevated.

Two parallel narratives are unfolding. The first is political: Whether Warsh aligns with the Trump administration’s preference for lower interest rates or maintains the Fed’s institutional independence. The expectation is that he adheres to orthodoxy, but the question itself will linger over the proceedings.

The second, and more consequential, is balance-sheet policy. Warsh has been a long-standing critic of the Fed’s $6.7 trillion balance sheet – the legacy of successive rounds of quantitative easing. His approach to unwinding that portfolio, and the implications for funding markets, liquidity, and financial stability, will be central. This is not a theoretical debate; it is one that will shape the cost and availability of capital for years.

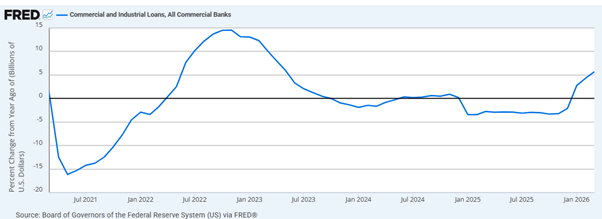

Away from Washington, the more important macro development is unfolding quietly within the banking system.

After nearly two years of stagnation, U.S. bank balance sheets are expanding again. From January 2024 through late 2025, loan growth was either negative or running at its slowest pace since the aftermath of the Global Financial Crisis. That regime has now shifted.

Recent bank earnings flagged a clear reacceleration in both loan and deposit growth — a trend confirmed by the Federal Reserve’s H.8 data, which tracks commercial bank activity in near real time.

5-year chart: Percent change (YoY) in US Commercial and Industrial loans

The composition of that growth is critical.

Deposits are once again expanding, but unlike the 2020–21 period, this is not being driven by central bank liquidity. Then, balance sheet expansion was a byproduct of aggressive quantitative easing, with liquidity largely recycling into reserves and government securities. As policy reversed through quantitative tightening and higher rates, that excess liquidity was withdrawn.

Today, the mechanism is fundamentally different.

Deposit growth is now being driven by credit creation. Loan growth has accelerated meaningfully, with core lending expanding at an annualised pace of more than 8% over the past three months. Within that, commercial and industrial (C&I) lending has been particularly strong, running above 20% annualised.

This matters because C&I lending is directly linked to real economic activity – funding working capital, capital expenditure, and inventory accumulation. In other words, this is not passive balance sheet expansion; it is an active impulse to nominal GDP.

The implication is straightforward: Financial conditions may not be as restrictive as headline policy rates suggest.

The shift from liquidity-driven to credit-driven growth carries different market implications.

On the one hand, it is supportive. Strong credit creation sustains spending, investment, and earnings, reinforcing the current growth cycle and underpinning risk assets.

On the other hand, it raises familiar late-cycle questions. Credit expansions at this stage of the cycle often coincide with rising leverage and a gradual build-up of financial vulnerabilities — particularly when increasingly intermediated through private credit and less transparent channels.

The balance, for now, remains constructive. Liquidity is still growing, but it is being created endogenously by the private sector rather than injected by central banks. That is a powerful, but ultimately more fragile, form of support.

Against this backdrop, geopolitical risk remains elevated but is being treated by markets with characteristic detachment.

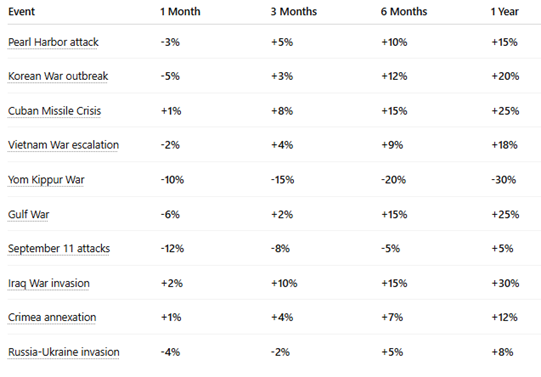

History provides a consistent pattern. Since the Attack on Pearl Harbor, major geopolitical shocks – wars, terrorist attacks, invasions – have triggered an initial drawdown in equities, typically in the range of 2–5% over the first month as uncertainty is priced.

What follows is more instructive.

S&P 500 performance after major geopolitical events

Source: ChatGPT

By three months, markets tend to stabilise and recover as clarity improves and policy responses emerge. By six months, gains often move into mid-to-high single digits. One year on, equities are typically meaningfully higher, frequently delivering double-digit returns as attention returns to earnings, growth, and liquidity.

The exceptions are equally revealing. The Yom Kippur War coincided with an oil embargo and a broader inflation shock, leading to a prolonged market downturn. Similarly, the aftermath of the September 11, attacks was compounded by an already weakening economic backdrop.

The lesson is clear: Markets are less sensitive to geopolitical events themselves, than to the macroeconomic conditions in which they occur.

Put differently, conflicts rarely derail equities unless they trigger something larger – an inflation shock, a recession, or a tightening in financial conditions.

The recovery in equities has been notable, but not excessive.

Despite a rally of more than +11% from recent lows, the S&P 500 is only up around +3% year-to-date. The tech-heavy NASDAQ has outperformed, rising approximately +17% from the lows and around +4% on the year.

What is striking is the absence of broad-based positioning excess. A classic “FOMO” phase – characterised by aggressive inflows and retail participation – has yet to materialise. That may yet emerge if geopolitical risks continue to fade and earnings remain resilient.

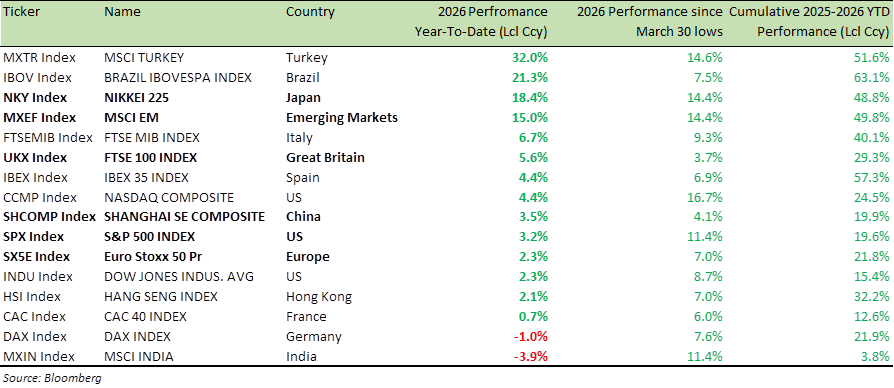

Global Equity Index Performance (2026 YTD, since March 30 to YTD and 2025-26 YTD)

US equities remain supported by a macro environment that is neither too hot nor too cold.

Growth continues at a modest pace, inflation has moderated significantly from its peak, and the labour market — at least on the surface — remains intact. This combination has underpinned the current rally and justified elevated valuations, particularly in quality growth and AI-linked sectors.

However, the underlying picture is more nuanced.

Growth has slowed from last year’s pace, hiring momentum has weakened, and a “jobless growth” dynamic is emerging. Inflation, particularly core, remains sufficiently sticky to keep the Federal Reserve cautious, maintaining a restrictive policy stance.

This creates a narrow path forward.

Earnings can continue to support markets if growth does not deteriorate sharply. But further valuation expansion becomes increasingly difficult in an environment where liquidity is constrained, and the cost of capital remains elevated.

The path to the S&P 500 at 8,000 and NASDAQ 100 at 30,000 remains intact, but it will not be linear. Periods of volatility, consolidation, and drawdowns are inevitable.

This is precisely the type of environment where structured strategies become relevant. Properly deployed, they allow investors to navigate volatility, define entry levels, and generate returns even in sideways markets.

The broader conclusion remains unchanged: Upside is intact, but increasingly dependent on earnings delivery rather than multiple expansion. Downside risks remain contained in the absence of a sharp deterioration in growth.

Staying long equities remains the core trade.

The next key inflection point lies externally. The upcoming Trump–Xi meeting in May will be critical, particularly for Chinese equities, which have lagged the global rally over the past two years.

For tailored strategies, stock-specific ideas, or structured solutions, please reach out to your relationship manager.

Best wishes,

Manish Singh, CFA