The US’s new tariffs have shaken up the global economy – but the AI boom is helping to hold things together

Summary

If two words were to define 2025, they’re tariffs and artificial intelligence. President Trump’s “Liberation Day” tariffs initially sent shockwaves through global markets. Economists warned of a sharp hit to trade, corporate margins, and global growth. Yet the anticipated recession never arrived. Instead, the S&P 500 is up over +16% year-to-date, and the Nasdaq has gained more than +20%, extending a powerful run driven by structural forces beneath the surface.

The reason? While tariffs tightened parts of the system, the AI boom expanded others. Corporate earnings have held up, risk appetite has returned, and productivity optimism is rising. Many of the most aggressive tariffs were ultimately scaled back or delayed – but AI’s momentum hasn’t paused. Markets are adjusting not to a collapse in global trade, but to a recalibration of where and how future growth will emerge.

AI is now being recognised as a true general-purpose technology — with potential long-term productivity gains of +1.5% to +3% annually. As compute costs decline and adoption accelerates, the path to profitability becomes clearer. Challenges remain: Tariff-linked inflation, fiscal drag, slower AI capex, or geopolitical shocks could all weigh on sentiment.

But the clear lesson from this cycle is that structural tailwinds have consistently outpaced short-term noise. Staying invested – especially through periods of technological transformation – remains the most effective strategy for compounding long-term wealth.

Tinsel, Trust, Tail Risk, & AI: The Markets Hidden in Christmas Classics

It’s almost that time of year again – market activity is slowing down, Radio Times in hand, and the annual ritual of deciding which Christmas movies to watch over the holidays. We all have our favourites: It’s a Wonderful Life, A Christmas Carol, Home Alone, Love Actually, and in my daughter’s case, The Grinch (the 2018 Pharell Williams version).

Christmas movies often feel like warm, nostalgic escapes from reality – but look closely and many of them are built on themes straight out of financial markets: Risk, fear, liquidity crunches, moral hazard, irrational behaviour, asset bubbles, and the psychology that drives economic cycles.

It’s a Wonderful Life — Liquidity Crunches & Bank Runs

George Bailey’s Building & Loan is a textbook lesson in liquidity risk: Long-term assets, short-term liabilities, and a sudden loss of confidence that sparks a classic bank run. A reminder that markets run on trust — until they don’t.

A Christmas Carol — Behavioural Finance in Victorian Clothing

Scrooge is the original case study in loss aversion, hoarding, and over-saving at the expense of utility. The ghosts force him to confront future regret — essentially a crash course in long-term forecasting and behavioural incentives.

Home Alone — Risk Management & Tail Events

Kevin McCallister is an 8-year-old master of scenario analysis. He anticipates threats, allocates resources smartly, and creates asymmetric defences with limited capital. It’s tail-risk hedging… through marbles, nails, and paint cans.

The Santa Clause — Succession Risk & Governance Failures

Santa quite literally falls off the roof, and leadership transfers via a poorly drafted contractual clause. It’s corporate governance gone wrong — unclear terms, no oversight, and no succession planning.

The Grinch — Overconsumption & Sentiment Cycles

Whoville thrives on relentless consumption, leaving it vulnerable to a collapse in demand. The Grinch’s theft is a sentiment shock, showing that an economy built purely on cheer is only as strong as its confidence levels.

Well, we are not going to just talk about movies, so let’s look at the state of the market.

If 2025 can be summed up in two words, they are: Tariffs and Artificial Intelligence (AI).

The US’s new tariffs have shaken up the global economy – but the AI boom is helping to hold things together.

When US President Donald J. Trump rolled out his “Liberation Day” tariffs in April, many economists warned of a global shock. The consensus predicted US import slowdowns would choke global supply chains, hurt exports, stunt growth, and cost jobs around the world.

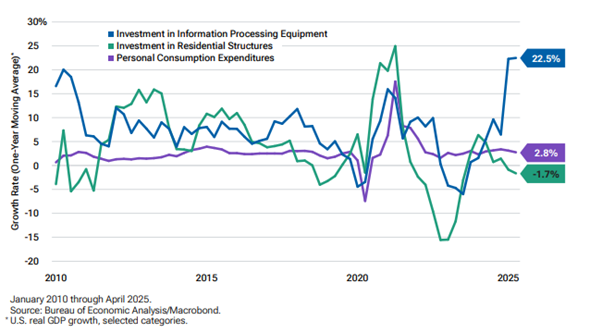

The AI infrastructure buildout is pulling the US economy up

Yet, months later, some of those same economists are revising their growth forecasts upward. Despite the tariff barrage, there’s been no recession, and markets are holding firm. The S&P 500 is up almost +16% year-to-date, while the Nasdaq Composite has surged more than +20%, building on two straight years of nearly +20% annual returns.

That resilience isn’t just luck – it reflects confidence in the AI-driven growth story, the resilience of corporate earnings, and a broader recalibration of risk across global capital markets.

In light of this, it’s often wiser to stay invested than to try to “time the market.” Trying to guess when markets will correct — pull out some money — and then jump back in is a high-stakes game. Instead, riding the upward trends, especially when structural themes like AI are driving value, tends to reward long-term discipline.

As Trump himself put it when defending the tariff strategy back in Spring: “We’re putting American workers and American innovation first.” Whether one agrees or not, the market seems to be voting with its capital — at least for now.

In short: Tariffs tightened one valve, but AI blew another wide open.

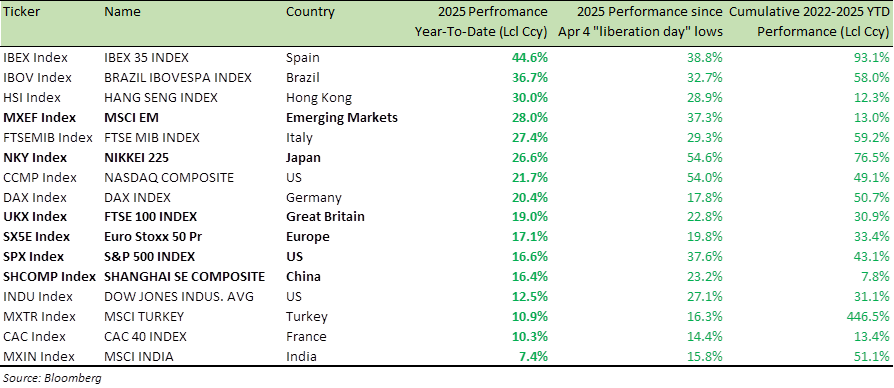

Global Equity Index Performance (2025 YTD, since April 4 YTD and 2022-25 YTD)

Last December in looking forward at 2025, I wrote:

“U.S. Equities Set for Uptick: Predicting specific figures is challenging, but U.S. stocks are well-positioned to see a rise of approximately 10-15% over the next year.”

I’d predict another double-digit year for 2026 for the S&P 500, as rates normalise and the job market improves. With a new Fed Chair in place probably by end of Q1, the year will be driven by robust growth, as inflation fear recede.

As for the next Fed chair, Polymarket gives Kevin Hassett a 74% chance of becoming the next U.S. Federal Reserve Chair. Hassett, Director of the National Economic Council since 2025, previously chaired the Council of Economic Advisers (2017–2019) and was a scholar at the conservative American Enterprise Institute. He has published widely on tax policy, growth, productivity, and macroeconomics.

In short, he is not a career central banker or regulator. His background is primarily that of an economic adviser, academic policy expert, and advocate for tax and growth-focused policies—experiences that strongly influence his economic philosophy and worldview.

If Hassett were appointed Fed Chair, his background and philosophy suggest several probable tendencies:

- Focus on growth and productivity, not just cyclical stabilization. He might push the Fed to consider structural growth and long-term output potential as part of its mandate.

- Balanced monetary policy. Rather than swing widely between aggressive rate hikes and rate cuts, he might favour a more measured, long-horizon approach — especially if underlying growth and productivity remain resilient.

- Coordination (or at least compatibility) with pro-growth fiscal policy. Given his history of advocating for tax reform and deregulation, he may prefer monetary policy that stabilizes inflation while giving the private sector room to invest and grow.

- More predictable, less politically reactive style. Coming from a policy-adviser and academic background, Hassett may favour rules-based or transparent frameworks over short-term discretion.

All this bodes well for risk assets.

On another note, Japan is coming up for discussion given its large pile of debt and rising inflation. It is also coming up in news for another reason – Trump called Prime Minister Sanae Takaichi last month, and advised her not to provoke Beijing on the question of Taiwan’s sovereignty.

Let me address the two issues – debt and inflation, and Taiwan, one at a time.

On debt, inflation and rising Japanese Govt bond (JGB) yield the central claim of a viral post “Japan printed money for 30 years and exported it to keep mortgages cheap, stocks inflated, and governments solvent,” is false and misleading.

Japan’s global financial strength comes from decades of persistent current account surpluses, not money printing. Its Net International Investment Position—around $3.4 trillion and ~80% of GDP—makes it one of the world’s largest creditor nations, alongside Germany.

Recent JGB movements reflect normal market dynamics, like reduced BoJ purchases and changing domestic investment needs, not economic collapse.

Myths about Japan or China dumping U.S. Treasuries are illogical, as it would destroy their own portfolios.

Doom narratives persist because fear sells, but Japan remains a rich, stable, globally integrated economy. Rising interest costs are manageable relative to nominal growth, and warnings of collapse are often biased and superficial.

30-Year Japan government bond (JGB) yield: 30-year price chart

Source: Bloomberg

On the topic of Japan’s growing support for Taiwan, it behoves the new PM to be more careful as it cannot count on US unconditional support under President Trump or the next resident of the white House.

There’s an old strategic truth worth revisiting: The decline of your patron is far more lethal than the rise of your rival.

Japan is more at risk from losing its patron – the US than from the rise of its rival China.

For decades, the US has been the world’s ultimate stabiliser – the patron state underpinning global security, trade, and financial architecture. Its consumer market absorbed global exports; its dollar anchored the monetary system; its military and diplomatic presence kept regional tensions from spiralling.

A rival’s rise – whether China, India, or any emerging power – is disruptive but manageable. The system can adjust to new competitors. Markets can reprice. Supply chains can evolve.

But the weakening of the anchor power?

That’s a different order of risk and needs to be responded with urgency.

Arguably, Prime Minister Takaichi has the toughest job of all the world leaders.

A rival adds pressure. A patron’s decline shakes the foundation and forces you to get off your back and become more proactive, creative, thoughtful and think anew.

As the world edges toward a more multipolar, more uncertain equilibrium, this asymmetry is becoming harder to ignore – in markets, in geopolitics, and in boardrooms.

The question for 2026 and beyond isn’t simply who is rising. It’s what happens if the system’s cornerstone begins to slip.

Former British Prime Minister Winston Churchill once said – “Peace is made secure not by the balance of forces, but by the strength of the strongest.”

With the US slipping, its priorities changing, the part of the globe that relied on US support, needs to rethink its strategy.

Looking Ahead: 2026–2027

The combination of tariffs and AI-driven investment is shaping not just 2025, but potentially the next several years of the economic cycle.

AI once grew more expensive, as models scaled, but efficiency gains have flipped that logic. Intelligence that cost $37 per million words in 2023 now costs only a few cents, thanks to faster chips, smarter code, leaner models, and open-weight competition. This cost collapse means every dollar now buys far more capability, accelerating adoption. Nvidia sits squarely at the centre: The NVL72 Supercycle—jumping from 8 GPUs per server to 72—is setting up multiple quarters of blowout results and could become one of the biggest tech cycles since the iPhone.

Tech adoption is also happening faster than ever. The flush toilet took 75 years to go mainstream; the smartphone took 10. Generative AI is on track to break every record. Roughly 40% of U.S. households already use AI at work or home, just two years after ChatGPT launched, and effective adoption rates may be far higher once embedded AI is included.

I believe that search behaviour will increasingly shift from traditional queries to AI chatbots. As ChatGPT releases a far stronger model trained on NVL72 Blackwell clusters at Microsoft, sentiment will swing back in its favour. Nvidia will benefit from this training wave, while fears that Google’s TPUs will meaningfully threaten Nvidia’s dominance remain overstated.

This shift will also hit digital advertising. A large share of ad spend will migrate from search engines to AI chatbots and emerging AI-native hardware. Google, long protected by its search monopoly, will face real competitive pressure, as user attention moves into conversational interfaces.

Inside companies, productivity gains will accelerate. AI is moving from “co-pilot” to “co-worker.” Knowledge workers will become dramatically more efficient as models adapt to proprietary data and custom workflows. Surveys show over 40% of firms already pay for AI services, and adoption is rising fastest across tech, finance, and professional services.

Barriers exist – regulation, legacy systems, tight budgets – but the shift from experimentation to deployment is unmistakable.

AI is the next great “general-purpose technology,” akin to electricity or the computer. Most economic estimates point to +1.5%–+3% annual productivity gains over the next decade—transformative in a world with slowing labour-force growth. The upside is huge, even if the full effect takes time to materialize. Profitability concerns are temporary. Compute gets faster and cheaper every year, and this trend is relentless. As costs fall and usage scales, today’s loss-making AI features will turn into highly profitable businesses.

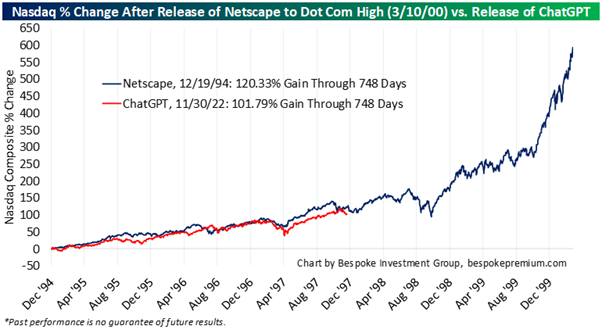

At the economy level, the US economy remains supported by strong earnings, pro-growth policies, active capital markets, and ongoing AI investment—benefits that are likely to ripple across global sectors. The major AI stock rally may still be ahead, potentially mirroring the trajectory of Netscape’s 1994 launch. So far, the pattern is strikingly similar (chart below).

That said, the equity markets are broadening. Leadership is moving beyond the AI mega-caps to companies building AI’s physical backbone and those set to benefit from sector rotation.

International and small-cap stocks are gaining appeal, fuelled by fiscal stimulus and improving global cyclical trends.

AI-related investment—spanning cloud infrastructure, chips, data centres, and automation—could drive double-digit earnings growth in large-cap tech through 2026.

Early enterprise AI adoption, highlighted by big tech CEOs in recent media appearances, points to a productivity surge not seen since the late 1990s. Coupled with re-shoring and structural investments in manufacturing, energy, and semiconductors, this makes annual S&P 500 gains of around +10% plausible, with the Nasdaq poised to lead.

Expansionary policies outside the US, especially in Germany, have been swift and significant. Aggressive easing by the European Central Bank, Bank of England, and emerging-market central banks further supports international equities.

Small caps stand to benefit the most as markets broaden beyond mega-cap tech and rates cuts in the US follow. Even modest flows away from the “Magnificent Seven,” could boost smaller stocks, which also thrive in lower-rate environments.

U.S. fiscal stimulus – including tax incentives for capex – backs growth, but policies like tariffs and immigration restrictions remain inflationary. With inflation near or above 3%, bonds may underperform, reinforcing equities as the preferred play.

I am a buyer of crypto – Bitcoin, Solana, and Ethereum. I view gold more as jewellery, though it still deserves a role as a portfolio hedge for when geopolitical risk become concern. I’m less convinced by illiquid private assets and believe structured equity investing, as we practice it, offers a better risk-adjusted path to generating 10–12% on an equity allocation.

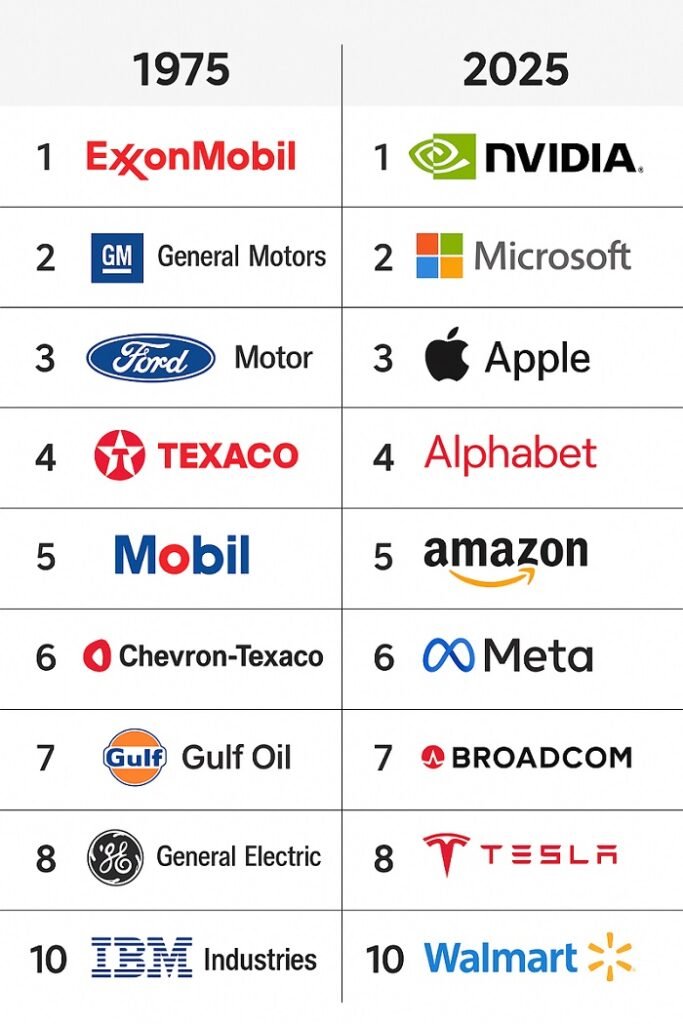

History shows that market leadership always evolves over time and revolve around themes.

None of the top 10 companies by market cap in 1975 remain in the top 10 today, and even from 2005, only Microsoft survives in the top 10 today.

Times for significant technological disruption tend to disrupt moats, we are in midst of it, but big tech has a big lead and over time they have consolidated their monopolistic position.

From Oil Titans to Tech Giants: Top 10 US Companies, 1975 vs 2025

Source: ChatGPT

What could disrupt all the positivity? Tariff-driven inflation, AI spending slowdowns, U.S. fiscal stress, and geopolitical shocks.

However, the lesson from 2023–2025 is clear – staying invested has consistently outperformed attempts to time the market, as structural themes like AI reward patience over precision. Time in the market, especially during technological inflection points, remains the most reliable path to long-term gains.

Markets aren’t just numbers – they’re stories about people navigating uncertainty, emotion, ambition, fear, and hope.

Never forget – investing is less about predicting the future and more about understanding human behaviour. And few things illustrate that better than the Christmas classics we return to every December. Because those movies beneath the sparkle and nostalgia, explore those same forces far more honestly than most investment textbooks or newsletters ( with possible exception of this one, I know I am biased)

Wishing you and your loved ones a joyful holiday season and a prosperous New Year. For those celebrating Christmas, may it be a wonderful celebration full of warmth and joy.

Best wishes,

Manish Singh, CFA